This analysis argues that Germany must immediately restart its three remaining nuclear facilities, Isar 2, Neckarwestheim 2, and Emsland which were shuttered in April 2023 despite operating licenses valid through 2024 and beyond.

The reopening of the Strait of Hormuz on April 17, 2026, following a fragile two-week ceasefire between the United States and Iran, has triggered a dangerous complacency in European energy policy circles. Oil prices have retreated from their $126 peak to approximately $98 per barrel, and the immediate threat of catastrophic supply disruption has temporarily receded .

Yet this reprieve is illusory. The underlying vulnerabilities exposed by the seven-week Hormuz closure during which approximately 20% of global oil supply and substantial LNG flows were severed remain fully intact. For Germany, the continent’s industrial powerhouse and largest electricity market, the crisis has precipitated a fundamental reconsideration of its 2023 nuclear phase-out.

This analysis argues that Germany must immediately restart its three remaining nuclear facilities Isar 2, Neckarwestheim 2, and Emsland which were shuttered in April 2023 despite operating licenses valid through 2024 and beyond. The confluence of persistent Middle Eastern instability, ongoing Russian aggression in Ukraine, the structural vulnerability of European LNG dependence, and the demonstrated unreliability of maritime energy chokepoints creates a strategic imperative that transcends the anti-nuclear consensus that has dominated German politics for two decades. The Hormuz crisis was not an aberration; it was a warning. And Germany, like Europe, remains unprepared for the next one.

The Fragile Ceasefire: Reading Between the Headlines

Yesterday’s Opening, Tomorrow’s Closure

The April 17 announcement by Iranian Foreign Minister Abbas Araghchi that the Strait of Hormuz is “completely open” for commercial vessels during the remainder of the two-week U.S.-Iran truce should provide cold comfort to energy strategists . The conditional nature of this opening explicitly tied to ceasefire adherence and coordinated routing by Iranian authorities renders it a political lever rather than a restoration of commercial freedom. As one senior Iranian official noted, keeping the strait open is “conditional on U.S. adherence to the terms of ceasefire,” with “significant differences” remaining on nuclear issues and sanctions relief .

President Trump’s assertion that Iran has “agreed to never again shut the Strait of Hormuz” and that “it will no longer be used as a weapon against the World” represents diplomatic aspiration rather than structural reality. Tehran’s capacity to close the strait through mines, anti-ship missiles, swarm boat attacks, or sabotage of coastal loading facilities remains undiminished. The Islamic Revolutionary Guard Corps retains extensive asymmetric capabilities specifically designed for maritime area denial. The fact that these weapons were not employed during the recent closure was a choice, not a constraint.

The ceasefire’s fragility is further evidenced by conflicting signals from regional actors. While Trump announced that Israel is “prohibited” from bombing Lebanon, Prime Minister Benjamin Netanyahu simultaneously declared that Israel has “not yet finished the job” against Hezbollah and that operations against the militant group were “still not complete” .

Israeli Defense Minister Israel Katz warned that residents returning to southern Lebanon “will have to be evacuated to allow completion of the mission” if fighting resumes . These statements suggest that the current truce is a tactical pause rather than a strategic settlement.

For European energy planning, this volatility carries profound implications. The International Energy Agency (IEA) estimates that restoring lost energy output from the West Asian conflict will take approximately two years, with variation by country Iraq requiring significantly longer than Saudi Arabia . This means that even under optimistic scenarios, global supply capacity remains constrained through 2028, amplifying the impact of any renewed disruption.

The Insurance Market’s Verdict

The maritime insurance sector’s response to the Hormuz reopening reveals professional skepticism regarding sustained stability. London shipping insurers, led by Beazley, have launched a $1 billion war cover consortium specifically for Hormuz transits, acknowledging that “complex and evolving situation” persists despite the ceasefire . War risk premiums, which spiked during the closure, remain elevated. This market-based assessment—made by entities with direct financial exposure to maritime risk contradicts the optimistic narrative of normalized energy flows.

The first loaded tankers to exit the Gulf since the U.S. blockade three Iranian vessels carrying five million barrels of crude departed on April 17, but these movements occurred under specific ceasefire conditions and Pakistani naval escort . The establishment of alternative routes, including South Korea’s successful Red Sea transit via Saudi Arabia’s Yanbu port, indicates that major energy importers are not betting on Hormuz stability. These contingency preparations, while prudent, add cost and complexity to global energy supply chains that will ultimately be reflected in European pricing.

Germany’s Energy Security Architecture: A House Built on Sand

The Post-Hormuz Reality Check

Germany’s energy position entering the 2026 crisis was structurally precarious, despite official narratives of successful diversification. The 2022 phase-out of Russian pipeline gas compelled by Moscow’s invasion of Ukraine was replaced not by genuine energy independence but by dependence on global LNG spot markets. When the Hormuz closure eliminated Qatari LNG flows (representing 12-14% of European LNG imports), Germany found itself competing with Asian buyers for limited alternative supplies, recreating the price dynamics that had devastated industrial competitiveness during the 2021-2023 energy crisis .

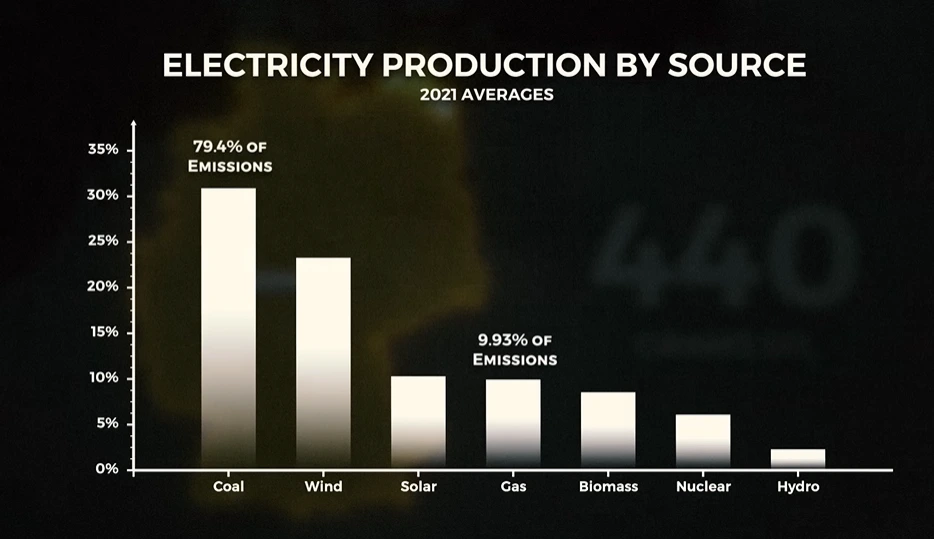

The German electricity grid’s specific vulnerabilities were exacerbated by the 2023 nuclear phase-out. The removal of 4.5 gigawatts of baseload nuclear capacity approximately 6% of Germany’s installed generation capacity forced increased reliance on coal-fired power plants and gas peakers precisely when gas supplies were constrained and prices surged. The environmental irony is stark: Germany’s anti-nuclear ideology, rooted in Green party politics and amplified by the Fukushima disaster, resulted in increased coal combustion during the 2026 crisis, raising carbon emissions while failing to ensure supply security.

The concurrent sabotage of the Nord Stream pipelines initially in September 2022 and potentially subject to renewed attack given ongoing geopolitical tensions demonstrates that Germany’s energy infrastructure faces multi-vector threats. The Nord Stream attacks, widely attributed to Russian state or proxy actors, revealed the vulnerability of undersea energy infrastructure to asymmetric warfare. With the Hormuz crisis demonstrating similar vulnerabilities for maritime supply chains, Germany confronts a strategic environment where neither pipeline nor seaborne energy flows can be assumed secure.

The Coal Trap

Germany’s response to the 2022 energy crisis extending the operational life of lignite and hard coal power plants provided short-term supply security at substantial environmental and economic cost. The country burned 44 million tons of lignite in 2023, the highest level since 2018, generating approximately 275 million tons of CO2 emissions. This “coal renaissance” directly contradicts Germany’s climate commitments while failing to address the structural vulnerabilities exposed by import dependence.

The 2026 Hormuz crisis has forced a similar, if more acute, choice. With gas prices spiking and renewable generation subject to weather variability, Germany’s grid operators have again relied on fossil thermal capacity to maintain stability. The International Monetary Fund (IMF) has explicitly warned European governments against excessive shielding of consumers from energy price spikes, noting that “prices help reduce demand and bring supply and demand back into balance” and that many proposed measures “weaken that signal” . Yet political imperatives in Germany, as elsewhere, favor intervention over market adjustment, perpetuating a cycle of subsidy and supply risk.

The Nuclear Option: Technical Feasibility and Strategic Necessity

The Three Reactors: Current Status

Germany’s three remaining nuclear power plants—Isar 2, Neckarwestheim 2, and Emsland—were not decommissioned due to technical obsolescence or safety failures. They were shuttered based on political decision-making that prioritized ideological commitment over engineering reality. At closure in April 2023, all three facilities held valid operating licenses and had undergone recent safety upgrades. Their removal from the grid was a policy choice, not a technical necessity.

The technical case for restart is robust. Nuclear power plants, unlike gas turbines or coal facilities, are not subject to fuel supply volatility. Uranium inventories, typically maintained for 12-24 months of operation, insulate reactors from short-term supply disruptions. While approximately 40% of global uranium production occurs in Kazakhstan, Canada, Australia, and Namibia provide politically stable alternative sources. France’s extensive domestic nuclear fuel cycle capabilities offer additional supply security within the European context.

Restarting the three reactors would restore approximately 4.5 GW of baseload capacity, generating roughly 35-40 terawatt-hours annually—equivalent to approximately 10% of Germany’s current electricity consumption. This generation would displace an equivalent volume of coal and gas-fired power, reducing carbon emissions by an estimated 30-40 million tons annually while providing grid stability services that intermittent renewables cannot match.

The Regulatory and Political Barriers

The primary obstacles to nuclear restart are political and regulatory rather than technical. Germany’s Atomic Energy Act was amended in 2022 and 2023 to eliminate nuclear power, requiring legislative reversal to enable resumption of operations.

The current coalition government, comprising Social Democrats, Greens, and Liberals, maintains formal commitment to the nuclear phase-out, though the Liberals have historically been more sympathetic to nuclear power than their coalition partners.

The political calculus, however, is shifting. The 2026 energy crisis has exposed the fragility of Germany’s energy security model, with industrial associations and labor unions increasingly vocal about competitiveness concerns.

The Federation of German Industries (BDI) has warned that sustained high energy costs threaten “deindustrialization” in sectors including chemicals, steel, and automotive manufacturing. These pressures create political space for a reconsideration of nuclear policy, particularly if framed as a temporary “bridge” measure rather than permanent reversal of phase-out commitments.

Regulatory re-licensing would require safety inspections, potentially fuel reloading, and workforce reconstitution. The German nuclear regulator (BNetzA) would need to certify restart safety, a process estimated at 6-12 months given the recent operational history of the facilities.

While not immediate, this timeline aligns with the IEA’s projection of two years for full regional energy supply recovery, suggesting that restarted reactors could contribute to a more resilient German energy position by 2027-2028.

Comparative Analysis: European Nuclear Strategies

France: The Nuclear Advantage

France’s energy security position during the 2026 crisis contrasted sharply with Germany’s, demonstrating the strategic value of nuclear power. With approximately 70% of electricity generated from nuclear sources, France maintained greater insulation from gas price volatility than its neighbor. While France faced increased costs for oil-fired peaking plants and some gas generation, the bulk of its electricity supply remained price-stable and domestically controlled.

French President Emmanuel Macron’s announcement of expanded naval operations in the Strait of Hormuz part of Operation Aspides further illustrates the geopolitical leverage conferred by energy independence . France’s ability to project military power to secure energy supply routes stems partly from the reduced domestic vulnerability that nuclear power provides. Germany, by contrast, faces the uncomfortable choice between accepting supply risk or participating in potentially escalatory military operations to secure foreign energy sources.

Belgium and the Netherlands: Reversal Precedents

Belgium’s 2023 decision to extend the operational life of two nuclear reactors (Doel 4 and Tihange 3) through 2035, reversing previous phase-out commitments, provides a direct precedent for German policy reconsideration. The Belgian reversal was driven by nearly identical concerns supply security following the Ukraine invasion and recognition that renewable capacity could not substitute for baseload generation on planned timelines.

The Netherlands has similarly delayed nuclear phase-out plans, while Poland pursues ambitious new nuclear construction with American and South Korean technology partners. These national decisions reflect a broader European reassessment of nuclear power’s role in energy security, with Germany increasingly isolated in its absolute rejection of the technology.

The Strategic Case: Beyond Electricity Generation

Industrial Competitiveness and Hydrogen

Germany’s industrial decarbonization strategy depends heavily on green hydrogen produced via electrolysis powered by renewable electricity. This “Power-to-X” approach, while theoretically sound, assumes abundant low-cost electricity that the 2026 crisis has shown to be unreliable. Nuclear power offers an alternative hydrogen production pathway, pink hydrogen via high-temperature electrolysis or thermochemical processes that is dispatchable and independent of weather conditions.

The chemical industry, concentrated in Germany’s Rhineland and Saxony regions, requires stable, high-volume energy inputs that intermittent renewables cannot guarantee. BASF, the world’s largest chemical producer, has warned that European energy costs threaten the viability of major production facilities. Nuclear restart would provide competitive electricity and process heat, preserving industrial employment and export capacity while advancing decarbonization objectives more effectively than the current coal-dependent reality.

Grid Stability and Renewable Integration

Germany’s renewable energy expansion while substantial in capacity terms has created grid management challenges that nuclear power could help address. The variability of wind and solar generation requires either storage (currently inadequate at scale), demand response (limited industrial flexibility), or dispatchable backup (currently fossil-fueled). Nuclear reactors provide inertia and frequency regulation services that stabilize grids with high renewable penetration, potentially enabling faster renewable expansion rather than hindering it.

The 2026 crisis demonstrated that Germany’s current grid configuration, heavily dependent on fossil backup for renewable variability, is vulnerable to fuel supply disruptions. Nuclear restart would provide a non-fossil dispatchable foundation, reducing the gas and coal capacity required for system reliability and thereby diminishing exposure to the import risks that the Hormuz closure exemplified.

Objections and Counterarguments

Safety Concerns

Opponents of nuclear restart will cite safety risks, referencing Fukushima and Chernobyl. These concerns, while emotionally resonant, mischaracterize the risk profile of modern Western reactor designs. Germany’s remaining plants are Generation II+ facilities with extensive safety upgrades, including containment structures and redundant cooling systems that were absent at Chernobyl and inadequate at Fukushima. The European Union’s stress tests, conducted following Fukushima, confirmed the safety of these facilities under extreme scenarios including earthquake, flooding, and loss of external power.

Statistical risk assessment favors nuclear power over continued coal combustion, which causes approximately 13,000 premature deaths annually in Germany through air pollution, and over the climate risks of sustained fossil fuel dependence. The 2026 crisis, by forcing increased coal burning, has likely caused more immediate health impacts than the hypothetical risks of nuclear operations.

Proliferation and Waste

Nuclear waste management remains unresolved in Germany, with no operational permanent repository and ongoing controversy regarding interim storage. However, the waste inventory from three additional years of operation is marginal compared to existing legacy waste, and the political imperative to resolve storage questions exists regardless of restart decisions. The Konrad repository, under construction in Lower Saxony, is scheduled to open in 2027 and could accommodate low and intermediate-level waste from continued operations.

Proliferation concerns are irrelevant to the German context; Germany is a Nuclear Non-Proliferation Treaty member with comprehensive safeguards and no weapons program. The uranium supply chain, while concentrated in certain producer states, is less politically volatile than the gas supply chains that Germany has accepted from Russia and Qatar.

Economic Viability

Critics argue that nuclear power is economically uncompetitive with renewables. This assessment relies on levelized cost calculations that exclude system integration costs and security externalities. The 2026 crisis revealed the true cost of supply insecurity: industrial production curtailments, price volatility, and strategic vulnerability. When these factors are included, nuclear power’s baseload reliability and fuel supply stability represent economic advantages rather than liabilities.

Furthermore, the sunk costs of Germany’s nuclear infrastructure—already constructed, licensed, and recently operational—create a unique economic case for restart that does not apply to new construction proposals. The marginal cost of extending operations for existing facilities is substantially lower than building equivalent renewable capacity with storage or maintaining fossil backup capacity.

The Path Forward: Policy Recommendations

Immediate Actions (0-3 Months)

The German government should commission an independent technical assessment of restart feasibility for Isar 2, Neckarwestheim 2, and Emsland, conducted by the Federal Office for the Safety of Nuclear Waste Management (BASE) and the Reactor Safety Commission (RSK). This assessment should evaluate physical plant condition, workforce availability, fuel supply, and regulatory requirements for resumption of operations.

Concurrently, the government should initiate legislative preparation to amend the Atomic Energy Act, enabling restart under specific conditions tied to energy security imperatives. This legislation should include sunset provisions—perhaps 10-year operational extensions—to maintain political commitment to eventual phase-out while addressing immediate security needs.

Medium-Term Measures (3-12 Months)

Assuming positive technical assessment, restart preparations should commence including workforce retraining, supply chain reactivation, and regulatory relicensing. The government should negotiate with plant operators (PreussenElektra, EnBW, RWE) regarding operational contracts and liability frameworks.

Germany should coordinate with France and other nuclear-capable EU members to develop a European strategic uranium reserve, reducing supply chain vulnerabilities and enhancing collective bargaining power with producers. This initiative would parallel existing EU strategic oil and gas storage mechanisms.

Structural Reform (1-3 Years)

The 2026 crisis should prompt a fundamental reassessment of German energy security doctrine, moving from source diversification to structural resilience. This includes maximizing indigenous generation (renewables, nuclear, and potentially North Sea gas), enhancing storage capacity, and developing demand-side flexibility. Nuclear restart should be positioned within this broader resilience framework, not as an isolated measure but as a component of a diversified, secure energy system.

The False Choice of Ideology

The reopening of the Strait of Hormuz provides temporary relief but no strategic security. The ceasefire is fragile, the underlying conflicts unresolved, and the demonstrated capacity for supply disruption undiminished. Germany’s energy policy, predicated on the assumption that global markets will reliably deliver affordable supply, has been proven dangerously optimistic.

The nuclear phase-out of 2023 was a political decision made in conditions of perceived energy security that no longer obtain. Reversing this decision is not an admission of failure but an adaptation to changed circumstances a hallmark of responsible governance. The reactors at Isar, Neckarwestheim, and Emsland represent stranded assets of immense strategic value, capable of providing clean, secure, baseload power that Germany desperately needs.

The choice is not between nuclear and renewables; Germany requires both to achieve climate objectives and security imperatives. The choice is between energy realism and energy ideology, between acknowledging vulnerabilities and pretending they do not exist. The Hormuz crisis was a warning. Germany should heed it while the opportunity for preparation remains.

The alternative, continued reliance on volatile global markets, fossil fuel backup, and wishful thinking about renewable timelines invites repetition of the 2026 crisis with potentially more severe consequences. Nuclear restart is not a panacea, but it is a necessary component of a secure, decarbonized, and competitive German energy system. The time for political courage is now, before the next crisis demonstrates the cost of complacency.

Sources: This analysis draws upon official statements from the Iranian Foreign Ministry, U.S. Presidential communications, IEA assessments, IMF policy guidance, and maritime insurance market data. Technical specifications regarding German nuclear facilities are based on Bundesnetzagentur documentation and operator reports. Market data reflects conditions as of April 18, 2026.

#EnergySecurity #NuclearPower #StraitOfHormuz #GermanPolitics #Energiewende #OilPrices2026 #LNG #Geopolitics